For many small business owners, month-end can feel overwhelming. Transactions pile up, accounts need reconciliation, and financial reports must be reviewed. However, a structured month-end closing process helps ensure accurate financial records, better cash flow management, and informed business decisions.

A well-executed month-end close allows businesses to identify errors, monitor performance, and stay prepared for tax season. Whether you manage your books in-house or work with an Outsourced Bookkeeping in the USA team, following a consistent checklist can save time and reduce costly mistakes.

What Is a Month-End Close?

A month-end close is the process of reviewing, reconciling, and finalizing all financial transactions for a specific month. The goal is to ensure that financial records are complete, accurate, and ready for reporting.

By closing your books monthly, you can:

- Maintain accurate financial statements

- Detect accounting errors early

- Improve cash flow visibility

- Simplify tax preparation

- Support better business decisions

- Strengthen financial controls

Why Month-End Closing Is Important

Many small businesses wait until quarter-end or year-end to review their finances. Unfortunately, this approach can lead to overlooked errors, missing transactions, and financial surprises.

A monthly close helps business owners:

- Understand profitability in real time

- Monitor spending trends

- Track outstanding invoices

- Manage liabilities effectively

- Ensure compliance with accounting standards

Consistent month-end procedures create a solid foundation for financial success.

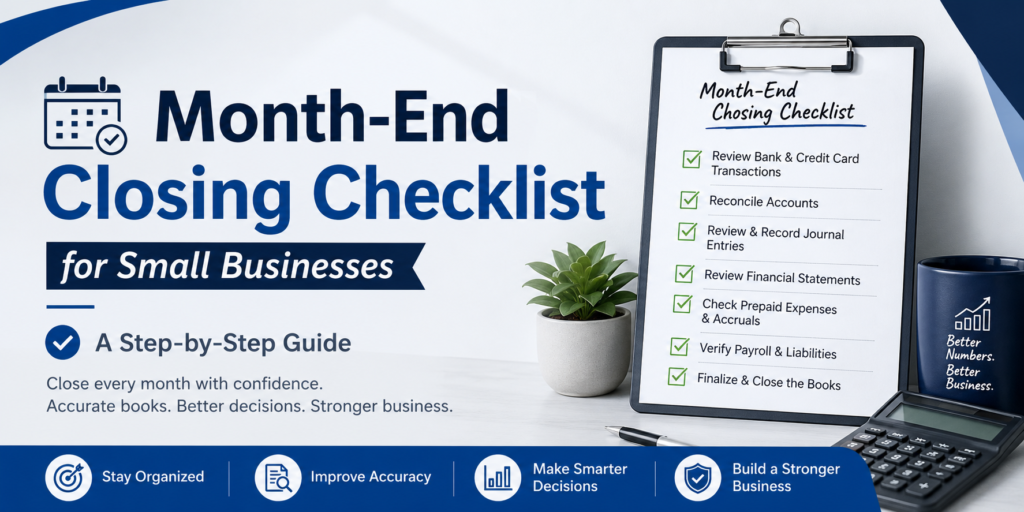

Complete Month-End Closing Checklist

1. Record All Financial Transactions

Before beginning the close process, ensure all transactions for the month have been entered into your accounting system.

Review:

- Sales invoices

- Customer payments

- Vendor bills

- Expense receipts

- Payroll entries

- Loan payments

- Credit card transactions

Missing transactions can result in inaccurate financial statements.

2. Reconcile Bank Accounts

Bank reconciliation is one of the most important month-end tasks.

Compare:

- Accounting records

- Bank statements

Identify:

- Missing deposits

- Duplicate entries

- Bank fees

- Interest income

- Unrecorded transactions

Any discrepancies should be investigated and corrected immediately.

Benefits of Bank Reconciliation

- Prevents fraud

- Detects bookkeeping errors

- Improves cash accuracy

- Supports audit readiness

3. Reconcile Credit Card Accounts

Review all business credit card statements and compare them with recorded transactions.

Verify:

- Charges are categorized correctly

- Receipts are available

- Personal expenses are excluded

- Outstanding balances are accurate

Failure to reconcile credit cards can significantly distort expense reporting.

4. Review Accounts Receivable

Accounts receivable represent money owed by customers.

Review:

- Outstanding invoices

- Aging reports

- Overdue balances

- Customer payment trends

Questions to ask:

- Which invoices are more than 30 days overdue?

- Are collection efforts needed?

- Are any balances uncollectible?

Keeping receivables current improves cash flow.

5. Review Accounts Payable

Accounts payable represent amounts owed to vendors.

Verify:

- All vendor invoices are entered

- Duplicate bills are removed

- Payment due dates are accurate

- Vendor balances match records

Timely payables management helps avoid late fees and strengthens vendor relationships.

6. Record Accrued Expenses

Some expenses may be incurred during the month but not yet paid.

Examples include:

- Utilities

- Payroll

- Interest expenses

- Professional service fees

Recording accruals ensures expenses are recognized in the proper accounting period.

7. Verify Payroll Transactions

Review payroll records for accuracy.

Confirm:

- Employee wages

- Payroll taxes

- Benefits deductions

- Bonuses and commissions

- Employer tax liabilities

Payroll errors can lead to compliance issues and employee dissatisfaction.

8. Review Inventory Levels

Businesses that carry inventory should conduct monthly inventory reviews.

Verify:

- Inventory counts

- Inventory adjustments

- Damaged or obsolete inventory

- Cost of goods sold calculations

Accurate inventory records support reliable profit reporting.

9. Update Fixed Asset Records

Review purchases of equipment, vehicles, furniture, and technology assets.

Ensure:

- New assets are recorded

- Disposals are removed

- Depreciation is calculated properly

Maintaining accurate asset schedules helps support tax reporting and financial statements.

10. Review Loan and Debt Accounts

Verify balances for:

- Business loans

- Lines of credit

- Equipment financing

- Credit card debt

Record:

- Principal payments

- Interest expenses

- Outstanding liabilities

This ensures liabilities are accurately reported.

11. Review Revenue Recognition

Confirm that revenue is recorded correctly.

Questions to consider:

- Have all earned revenues been recognized?

- Are deferred revenues properly tracked?

- Were customer refunds recorded accurately?

Revenue errors can significantly impact financial reporting.

12. Check Sales Tax Liabilities

Businesses that collect sales tax should verify:

- Taxable sales

- Sales tax collected

- Sales tax payable balances

Errors in sales tax reporting can result in penalties and interest assessments.

13. Review Expense Categories

Examine expense accounts for unusual transactions.

Look for:

- Duplicate expenses

- Miscategorized transactions

- Personal expenses

- Missing receipts

Accurate categorization improves financial reporting and tax compliance.

14. Analyze Cash Flow

Understanding cash flow is critical for business stability.

Review:

- Cash inflows

- Cash outflows

- Operating cash position

- Upcoming obligations

Questions to ask:

- Is there enough cash to cover upcoming expenses?

- Are collections keeping pace with spending?

Regular cash flow analysis helps prevent liquidity issues.

15. Generate Financial Statements

After reconciliations and adjustments are complete, generate key reports.

Profit and Loss Statement

Shows:

- Revenue

- Expenses

- Net income

Balance Sheet

Displays:

- Assets

- Liabilities

- Equity

Cash Flow Statement

Tracks:

- Operating activities

- Investing activities

- Financing activities

These reports provide a snapshot of business performance.

16. Compare Actual Results to Budget

Evaluate performance against financial goals.

Review:

- Revenue variances

- Expense variances

- Profitability trends

This analysis helps identify opportunities for improvement and supports strategic planning.

17. Investigate Unusual Variances

Look for unexpected changes such as:

- Significant revenue increases or declines

- Large expense fluctuations

- Unexpected cash shortages

- Abnormal account balances

Understanding variances helps prevent future issues.

18. Review Key Performance Indicators (KPIs)

Track metrics relevant to your business, such as:

- Gross profit margin

- Net profit margin

- Accounts receivable turnover

- Current ratio

- Cash conversion cycle

Monthly KPI reviews support data-driven decision-making.

19. Organize Supporting Documentation

Maintain organized records for:

- Receipts

- Invoices

- Contracts

- Payroll reports

- Bank statements

Good documentation simplifies audits and tax preparation.

20. Lock the Accounting Period

Once all reviews and adjustments are complete, close or lock the accounting period.

This prevents:

- Accidental changes

- Duplicate entries

- Reporting inconsistencies

A closed period helps maintain financial integrity.

Final Thoughts

Taxiq & Accounting Inc., we understand that an efficient month-end closing process is crucial for maintaining accurate financial records and supporting informed business decisions. Our experienced bookkeeping and accounting professionals help businesses streamline reconciliations, manage financial reporting, identify discrepancies, and ensure their books are closed accurately and on time each month. By partnering with Taxiq & Accounting Inc., business owners can reduce administrative burdens, improve financial visibility, strengthen compliance, and focus on growing their business with confidence.